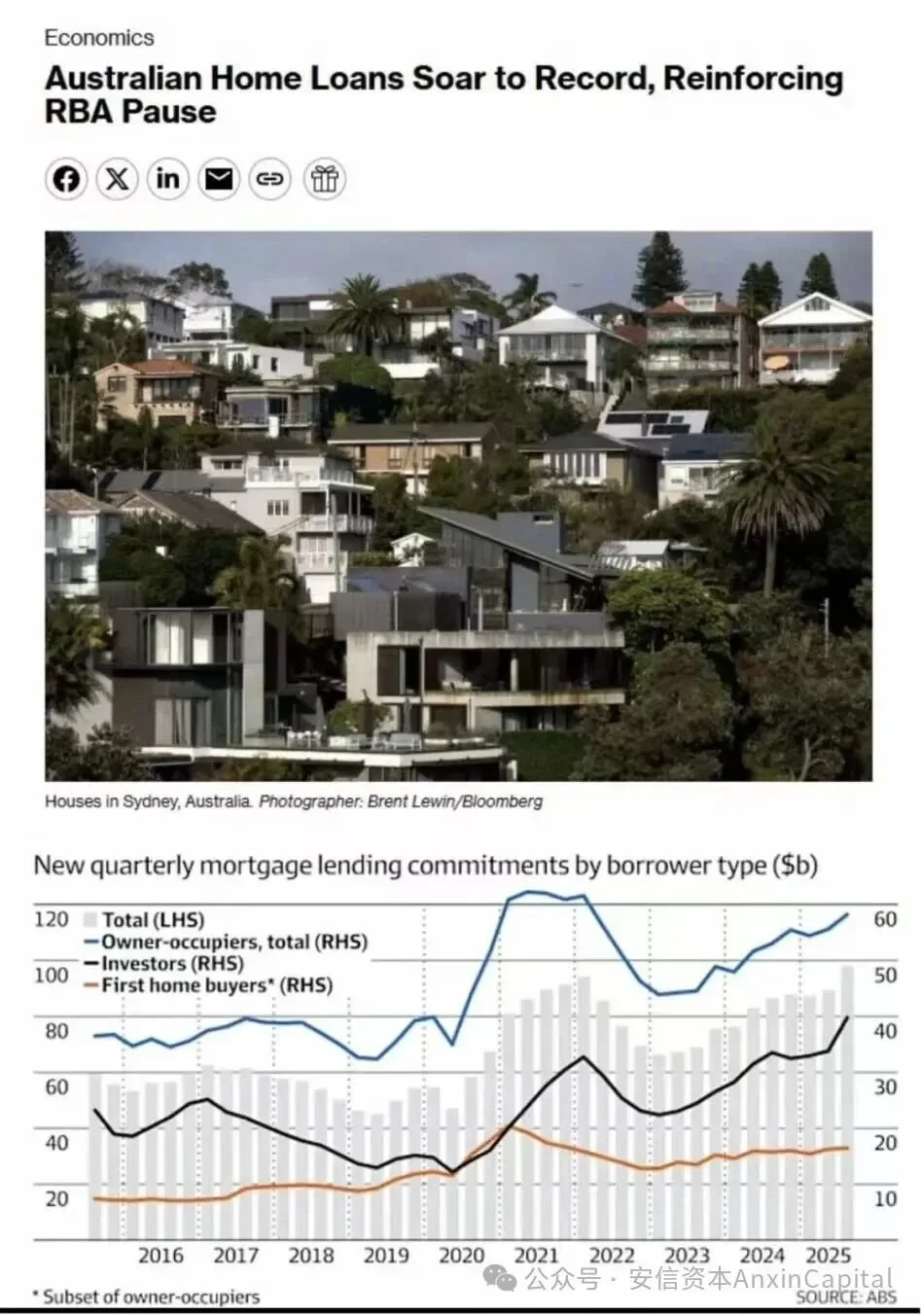

Recently, the Australian mortgage market has shown significant divergence. Against the backdrop of the Reserve Bank of Australia (RBA) clearly stating that it will not cut interest rates this year and keeping rates at 3.6%, owner-occupier loans have grown only moderately, while investor mortgages surged 17.6% year-on-year in the third quarter, marking the highest growth rate in nearly four years. Behind this 'counter-trend' phenomenon lies a complex interplay of demographic structure, policy incentives, and capital flows.

Market Status

According to the latest data from the Australian Bureau of Statistics (ABS), the total amount of new investment home loans in the third quarter of 2025 reached AUD 39.8 billion, accounting for 40% of all new home loans. It is worth noting that:

83% of investment loans flow into the secondary housing market, which does not increase the total supply of houses, but changes the rental market structure through ownership replacement.

-All states showed growth, with New South Wales (19%), Victoria (18.5%), and the Australian Capital Territory (27.8%) experiencing the most rapid increases. Queensland (11.9%) and Western Australia (9.1%) also maintained solid double-digit growth;

The average loan amount for investors rose to 686,000 AUD, an increase of 11,700 AUD compared to the previous quarter.

Driving force

1. Rent Yield Inversion and Holding Costs

Currently, the vacancy rates in Sydney and Melbourne are below 1.5%, with annual rent growth exceeding 10%, and net rental yields in some areas reaching 5%-7%. Even in the current interest rate environment, the positive cash flow characteristics still attract capital inflows.

2. Strengthening Long-Term Appreciation Expectations

Historical data shows that Australian real estate appreciates by an average of about 6%-8% per year (in core cities). In a context where inflation consistently exceeds 3%, tangible assets become a tool to hedge against the erosion of purchasing power.

3. Structural Easing of the Credit Environment

Although official interest rates remain high, some institutions have launched 40-year mortgages and 10-year interest-only products, indirectly lowering the threshold for monthly payments. Regulatory authorities have issued warnings but have not yet taken strong intervention measures.

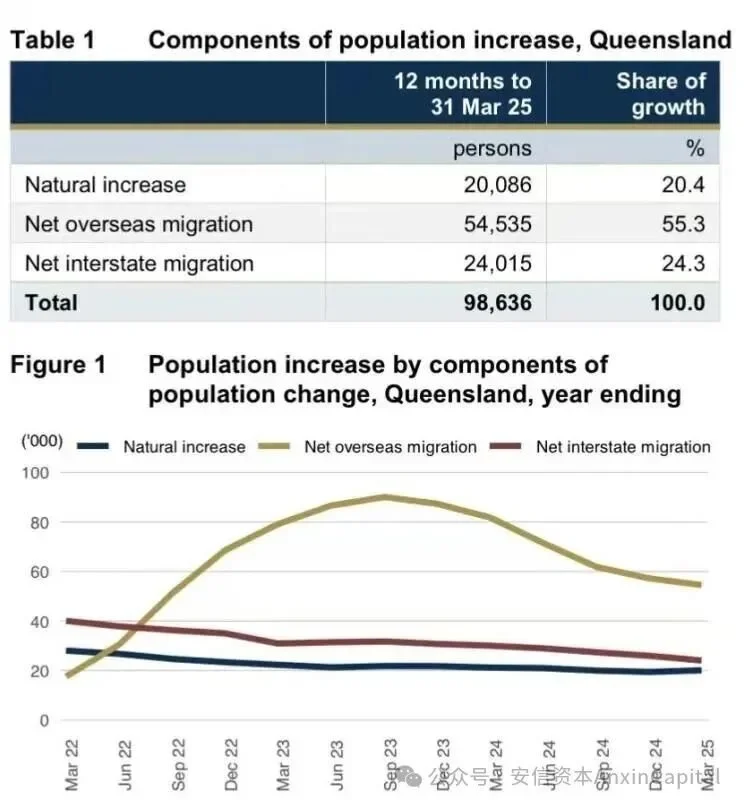

Regional differentiation, Queensland shows dual positive growth

While the investment boom sweeps across the country, Sydney is facing a severe structural population loss. According to in-depth analysis by the Australian Bureau of Statistics (ABS), over the past year, more than 100,000 (104,231) Sydney residents have net migrated to other parts of Australia. This figure, equivalent to 2% of the city's total population, makes Sydney the only first-tier city in Australia facing contraction due to the loss of local residents.

Sydney's population loss is not a cyclical fluctuation, but a structural trend driven by high living costs, a housing crisis, and urban development bottlenecks. So where is the population going? Queensland is the biggest beneficiary, attracting over 30,000 Sydney residents just last year. Many families trade the price of an apartment in Sydney for a house with a backyard and a coastal lifestyle in Brisbane or the Gold Coast, creating significant 'lifestyle arbitrage.'

-Interstate migration continues to flow in: According to the latest data for the third quarter of 2025, Queensland recorded a net interstate migration of 8,950 people for the quarter, an annual increase of 21.2%.

-Release of infrastructure dividends: Investments related to the 2032 Olympics are driving transportation upgrades, with cross-river railways and the Gold Coast light rail extension reshaping the city's framework.

- Rigid supply gap: Despite recent increases in housing prices, Brisbane's median is still only 60% of Sydney's, and the extended land development cycle further limits supply flexibility.

Trends and Market Alerts

Regulatory red lines and market overheating

- The proportion of investor loans has nearly reached APRA's historical intervention threshold (45%). If the growth rate continues, the reintroduction of loan growth restrictions cannot be ruled out.

- Concern over asset bubbles: the total value of real estate across Australia has exceeded 12 trillion AUD, equivalent to five times the GDP, with Sydney's house price-to-income ratio reaching 15 times;

-Structurally fragile, highly leveraged investors are sensitive to interest rate fluctuations. If a rebound in inflation forces the RBA to shift toward raising rates, it could trigger a sell-off.

From Cyclical Fluctuations to Structural Restructuring

- The federal government's '5% down payment program' has temporarily pushed up entry-level housing prices, but it is difficult to reverse the underlying supply and demand conflicts;

- Investors are shifting from purely residential properties to value-added assets (such as land plots and development projects), highlighting the land premiums in southeastern Queensland;

- If APRA tightens investor lending standards, the adjustment pressure in the Sydney and Melbourne markets will be significantly greater than in Brisbane and Perth, which are generally performing well.

Conclusion

The current uneven 'hot and cold' situation in the Australian housing market essentially reflects capital's vote on long-term population trends, infrastructure investment, and institutional stability. Against the backdrop of uncertain interest rate prospects, focusing on structural opportunities based on fundamentals—such as Queensland's ongoing demographic dividend and supply rigidity—may offer more certainty than chasing short-term fluctuations.