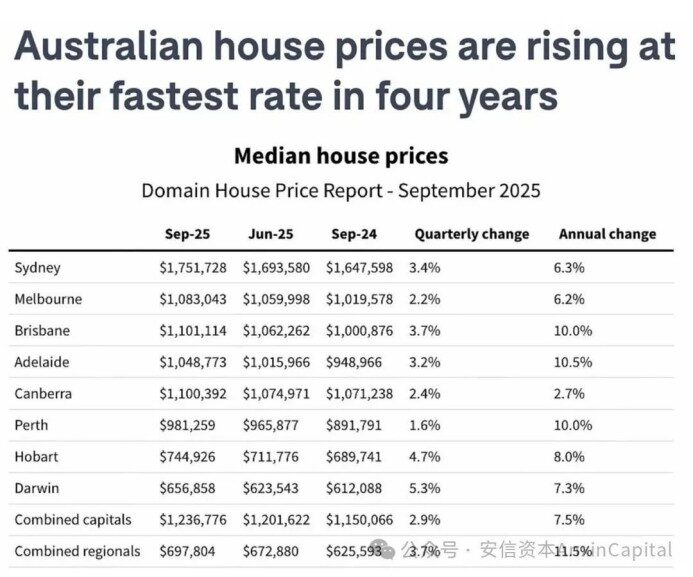

The latest data shows that the Australian real estate market is experiencing its strongest growth cycle in four years. According to Domain's third-quarter 2025 house price report, house prices in the eight major capital cities have all risen, with the median price for standalone houses in Sydney surpassing AUD 1.75 million to reach a new high. Brisbane, with a median price of AUD 1.1 million, has for the first time surpassed Melbourne, reshaping the pattern of the national housing market. At the same time, last week there were 3,448 auctions nationwide, reaching a four-year high, and market activity continues to heat up.

Policy and market resonance drive price increases

Monetary policy is loose

The Reserve Bank of Australia (RBA) has cut interest rates three times this year, bringing the cash rate down to 3.60%. This lowers mortgage costs and directly enhances residents' borrowing capacity. For a family with a loan of 600,000 AUD over 25 years, this rate cut in November can reduce their monthly payment by about 90 AUD; for a loan of 1 million AUD, it can reduce monthly payments by 150 AUD. This is not just numbers looking good—it is truly a "burden-reducing benefit" that allows many families to breathe a little easier.

Down payment policy expansion

The federal '5% Deposit Scheme' will, starting from October, remove the quota and income limits, and raise the property price caps for various cities, greatly lowering the entry threshold for first-time homebuyers. Data from the Commonwealth Bank of Australia (CBA) show that the number of conditional pre-approval applications for home loans has already significantly increased this year.

Concentrated demand release

With favorable policies combined with the peak season of spring sales, the auction clearance rate has remained above 70% for many weeks, and buyers are eager to enter the market.

The imbalance between supply and demand has become the core contradiction driving housing price increases.

Inventory is extremely scarce

The nationwide housing inventory on sale is equivalent to only 2.5 months of transactions, far below the healthy level of 3-4 months, and the supply-demand mismatch continues to worsen.

Supply target lag

The federal '1.2 million homes in five years' housing plan has already fallen behind by 50,000–66,000 units in its first year, with the slowdown in approval speed and insufficient construction efficiency restricting new supply.

Rental market squeeze

The vacancy rate is as low as 1.2%, and rising rents are pushing some tenants to turn to buying homes, further increasing demand pressure.

Regional differentiation intensifies, Brisbane performs outstandingly

The Rise of Brisbane

The median price of detached houses in Brisbane has reached 1.1 million Australian dollars, surpassing Melbourne for the first time to become the second most expensive capital city in Australia, and setting a record of 11 consecutive quarters of increases.

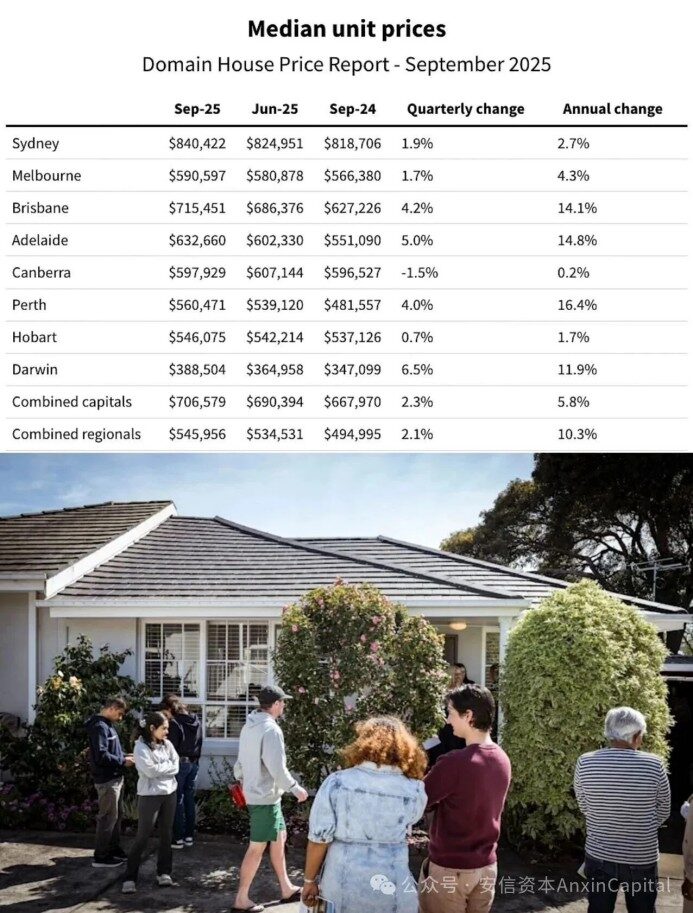

Apartment market leads the rise

Affordability pressures are driving demand towards apartments, with Brisbane apartment prices rising 4.2% quarterly, and the median surpassing 700,000 AUD.

Urban Hierarchy Reconstruction

Sydney (1.75 million AUD), Brisbane (1.1 million AUD), and Melbourne (1.083 million AUD) form a new price tier, while remote areas show a catch-up rise trend.

This shift reflects Brisbane's comprehensive advantages in population inflow, supply control, and livability, and the infrastructure expected for the 2032 Olympics is anticipated to further boost market confidence.

A market outlook with both risks and regulations

Policy adjustment space

APRA maintains a 3% repayment buffer threshold to curb excessive leverage; if credit overheats, it may activate macroprudential tools such as DTI.

Supply improvement is key

The medium- to long-term stability of housing prices depends on the pace of housing target implementation, and currently there are still bottlenecks in construction efficiency and infrastructure coordination.

Interest rate path uncertainty

Inflation stickiness and employment data will affect the RBA's subsequent decisions. If the interest rate cut cycle is interrupted, market demand may cool down.

Conclusion

The recent round of housing price increases has been driven by the dual forces of 'policy stimulus and supply shortage,' and mid- to short-term price resilience is expected to continue. Investors need to pay attention to regional differentiation trends, prioritize submarkets with clear population inflow and healthy supply-demand structures, and remain alert to policy shifts and liquidity risks.